Picking the Supply Number in a Crypto Valuation

How you pick a supply denominator moves a crypto valuation more than most other assumptions. Using HYPE as the worked example.

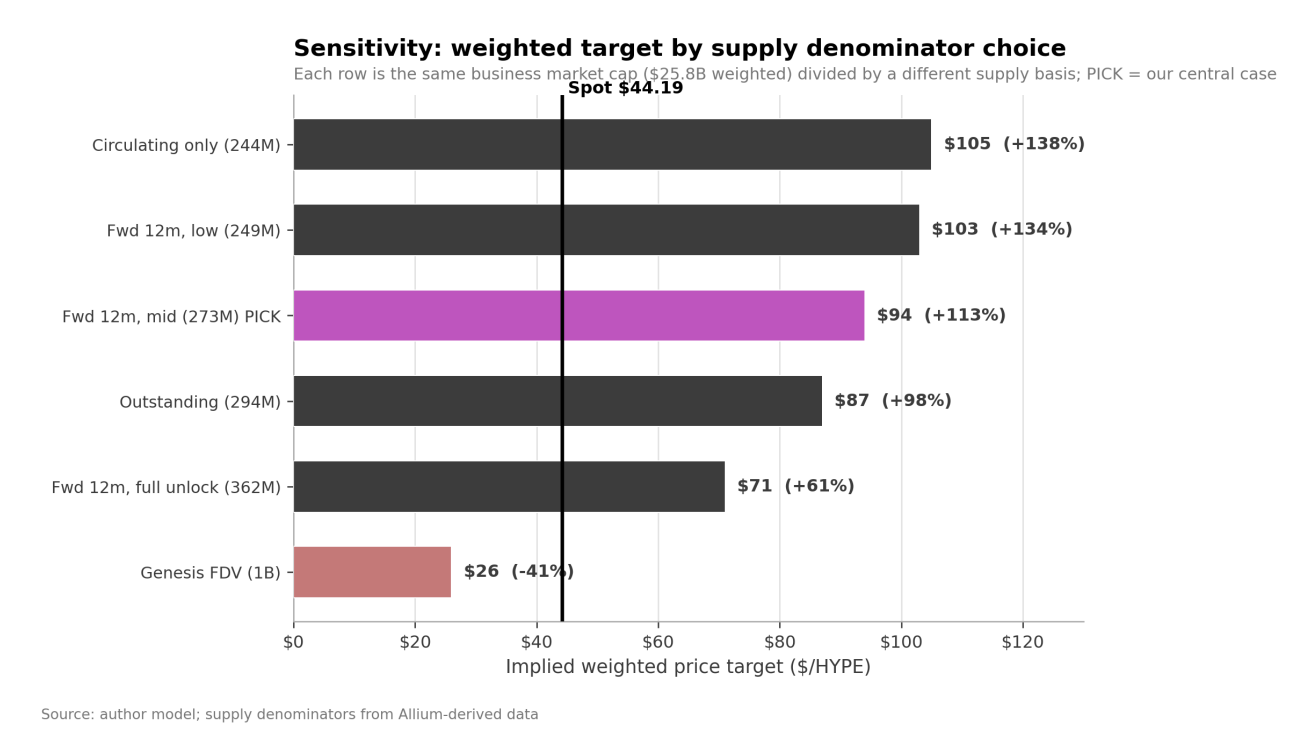

For HYPE, the same business value we estimate at $25.8B, divided across six

candidate supply numbers, produces price targets from $26 (FDV) to $105

(circulating only) per token. Same business, same revenue, same fee stream, and a

four-fold spread in the implied price driven entirely by the denominator.

We think FDV is the wrong supply number to anchor the analysis. Using FDV is like valuing Apple on its 50 billion shares authorized when the market values it on the 15 billion currently outstanding. The maximum-possible supply is rarely the supply that matters for the question being asked, and crypto should use the same playbook for projects building real businesses.

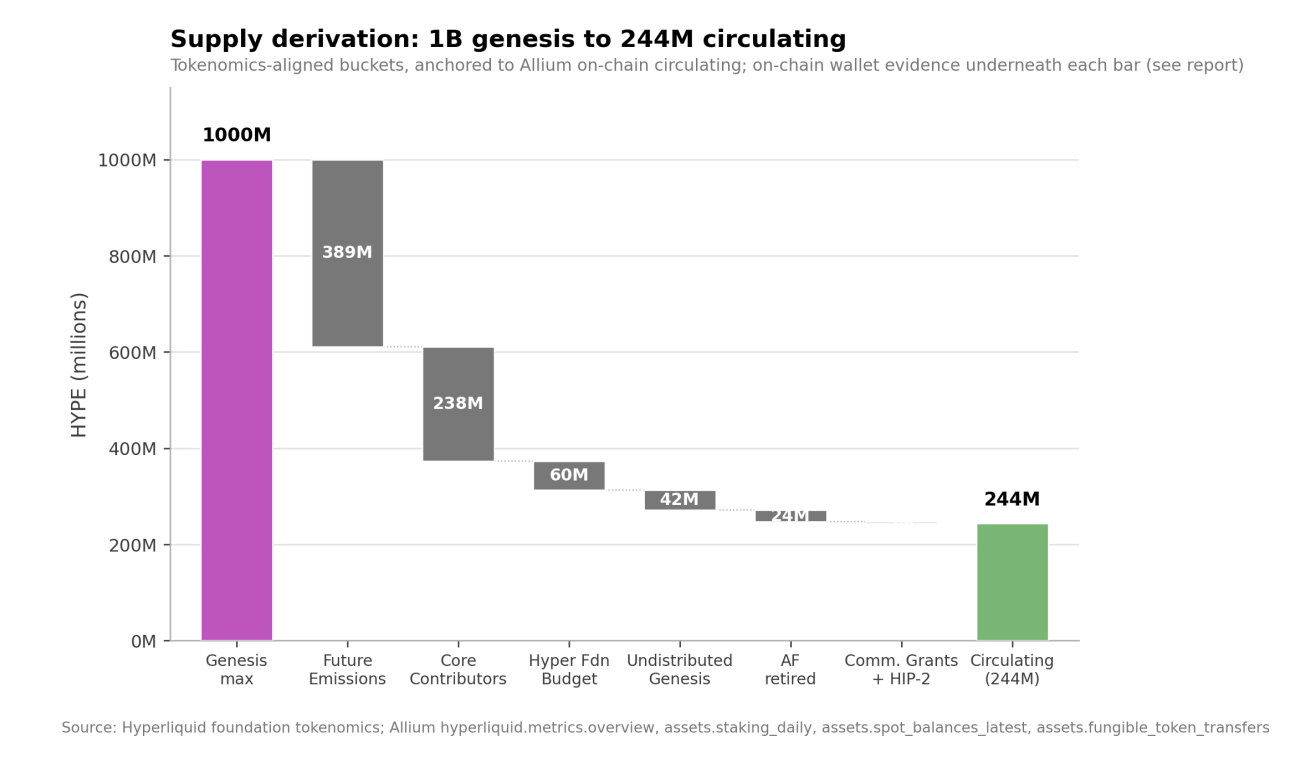

To see why, it helps to look at HYPE's supply mechanics directly.

Each non-circulating bucket has different mechanics. Lumping them together as "future dilution" misreads what is actually happening.

- Foundation reserves emit on a discretionary schedule.

- Locked Core Contributor tokens vest against the foundation's stated nonlinear policy.

- AF retired tokens are burned permanently.

- Undistributed Genesis sits with the protocol indefinitely.

HYPE's 1 billion genesis cap breaks down into 244 million circulating today and 756 million sitting across these buckets, each with its own clock and its own probability of ever entering the market.

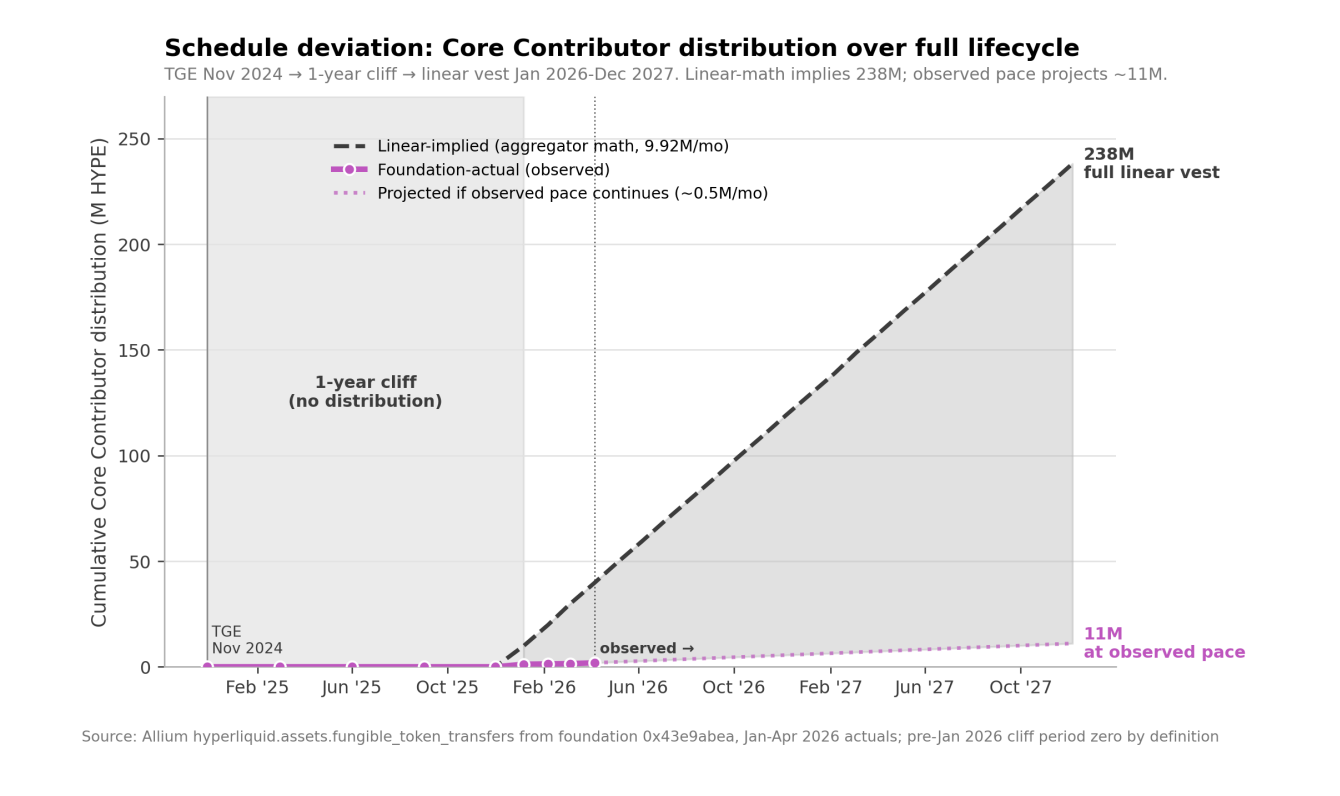

The bucket most often cited as the near-term risk, the Core Contributor schedule, makes the point most

clearly.

Linear vesting math is not gospel.The unlock cliff priced into the market is not the unlock happening onchain.

HYPE's 24-month Core Contributor allocation divided evenly across the window implies 9.92M tokens per month. Allium tracking of foundation main wallet outflows on the Jan 6 / Mar 6 / Apr 6 cliff dates shows 1.85M total distributed across four tranches, roughly 5% of the linear-implied rate. The foundation has publicly confirmed the schedule is nonlinear and discretionary.

If the largest, most-watched piece of the unlock calendar isn't behaving like the calendar suggests, the rest of FDV isn't going to behave like the maximum-supply math either.

FDV prices in every possible future issuance, and that isn't how we value anything else.

Apple has 50 billion shares authorized. The market values AAPL on the 15B currently outstanding, with forward expectations for buybacks and stock comp. Nobody divides Apple's market cap into 50B "just to be safe."

GameStop has more than doubled its share count since 2021 through repeated stock offerings. The market priced that dilution as it happened, not in advance based on maximum possible future issuance. A buyer who refused to touch GME because the company might someday issue 5x more shares would have missed the entire run.

Token issuers face the same cap-table incentives any equity issuer does. We can't predict precisely what a foundation will do with token supply over the long run, but game-theory-wise, dumping the entire allocation as fast as possible is the move of a memecoin, not a business with real fee revenue, a

buyback program, and 40K+ unique staking wallets. Crushing your own asset rarely makes sense.

FDV isn't always wrong. It's the right lens for ultra-long-horizon questions where eventual dilution matters, or for a memecoin-like project. For a 12-month price target on a token whose distribution is observably slow and is building a real business, it's the wrong tool for the question.

Which is why getting supply right matters more than most other modeling decisions in a crypto valuation. Allium onchain data infrastructure is what makes this kind of supply forensics tractable. The same tables behind this analysis are available to any team running serious onchain research.

This piece is informational and educational. It is not investment advice, financial advice, or a recommendation to buy, sell, or hold any digital asset. Cryptocurrency investments are speculative and involve substantial risk, including total loss of principal. Onchain figures sourced from Allium as of the publication date and may become stale. The author may hold positions in HYPE or related assets. Allium provides the underlying onchain data infrastructure used in this analysis. Readers should conduct their own due diligence and consult licensed financial professionals before making investment decisions.